Delivering Net Zero and a Clean Energy Economy

Header description

Australia’s transition to net zero will require a rapid scale-up of renewable energy generation, transmission and storage, supported by enabling infrastructure and the decarbonisation of construction and transport.

Renewable Generation

Around 90% of Australia’s GHG emissions come from burning fossil fuels for electricity, heating and transport.169 A significant transition in energy generation from fossil fuels to clean, renewable energy is required to achieve the 2035 target of a 62-70% reduction of GHG emissions below 2005 levels and net zero by 2050.

The Australian Government target of 82% renewable electricity by 2030 is a key milestone and the next five years are a critical timeframe. The nation’s two largest electricity grids – the NEM and the SWIS – now source more than 40% of electricity from renewables.170

Under the Step Change Scenario in the Australian Energy Market Operator’s 2024 Integrated System Plan (ISP), coal was expected to exit the market completely by 2037-38.xix In the Draft 2026 ISP, the Step Change Scenario retains coal until 2048-49. This adjusted timeline reflects the direction of the 2025 Queensland Energy Roadmap, as well as slower than previously planned closures of coal-fired power in New South Wales and Victoria. However, AEMO notes coal retirements may occur even faster than forecasted given higher operating and maintenance costs, more unplanned outages and greater renewable competition will challenge coal’s financial viability.

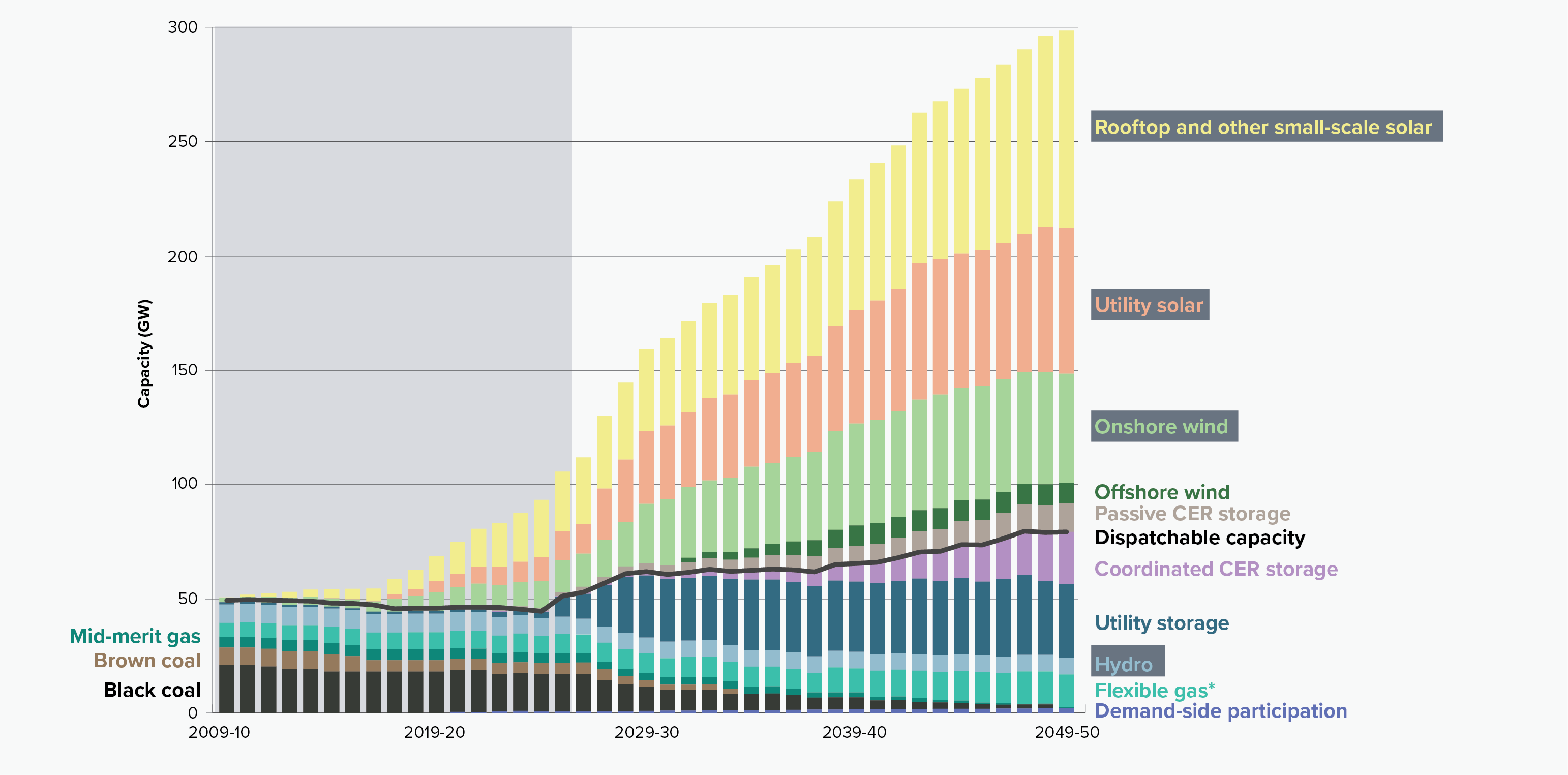

In Figure 3, under AEMO’s Step Change Scenario, the NEM will require a 422% increase in grid-scale wind and solar renewable energy, from 23 gigawatt (GW) in 2025 to approximately 120 GW, by 2050. This will be bolstered by 33 GW of storage and 14 GW of gas-powered generation.xx

Figure 3: Capacity, NEM GW 2009-10 to 2049-50, Step Change Scenario

Source: AEMO, Draft 2026 Integrated System Plan, Figure 1. N.B. “Rooftop and other small solar” includes forecast residential and commercial rooftop photovoltaic (PV) systems as well as larger distributed PV systems referred to as PV non-scheduled generation (PVNSG) systems. “Utility solar” also includes other distributed PV systems, optimised through the ISP assessment process. “CER storage” means consumer energy resources such as batteries and electric vehicles. “Flexible gas” includes gas-powered generation and potential hydrogen capacity.

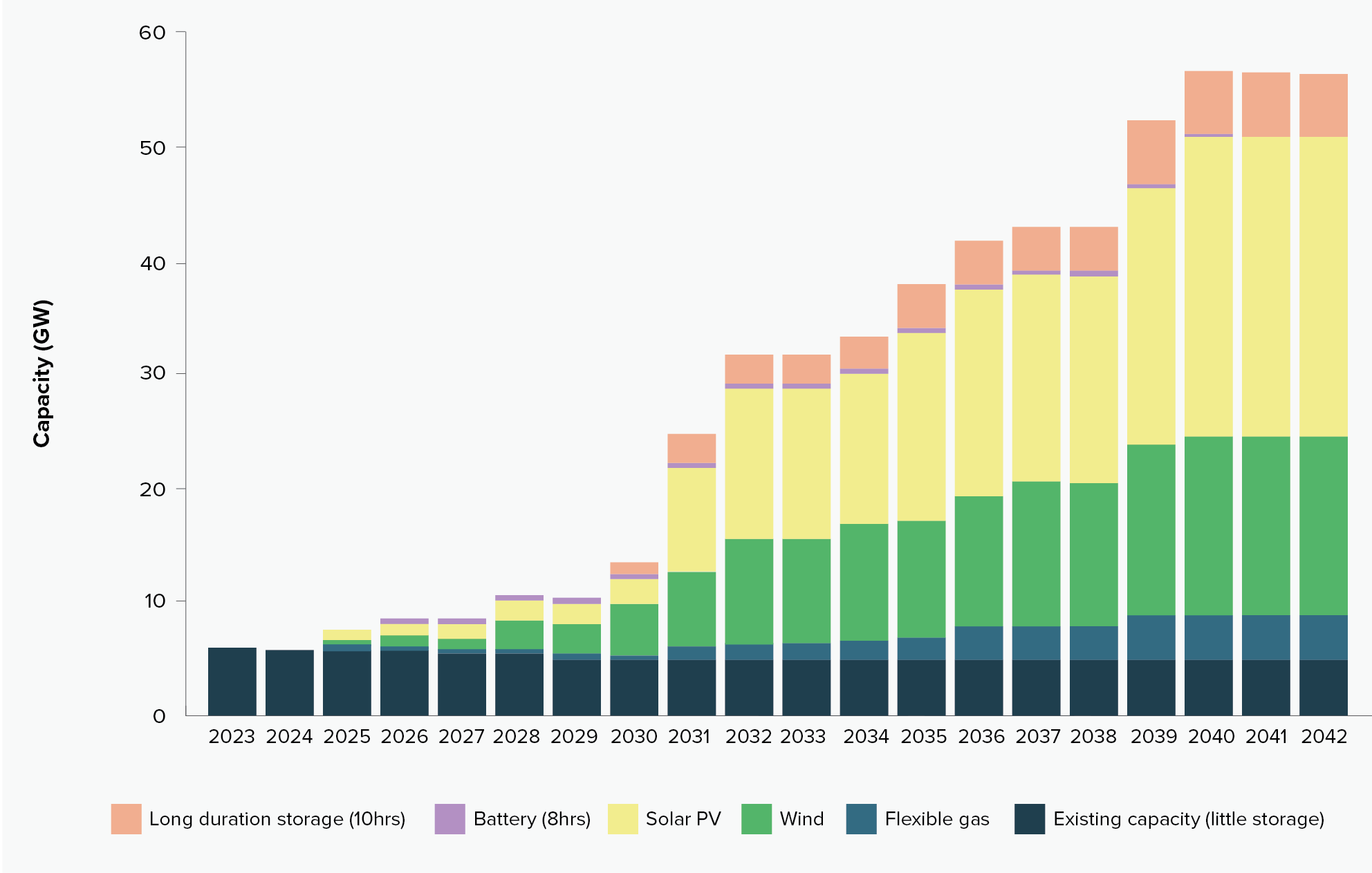

Similarly, the SWIS will require a 9-fold increase in wind and solar renewable energy, to approximately 42 GW, by 2042 (Figure 4). This will be firmed by approximately 5 GW of storage and 4 GW of gas-powered generation.

Infrastructure Australia’s 2025 Market Capacity Report shows that the unconstrained national pipeline of energy infrastructure, including transmission, solar, wind and pumped hydro projects is valued at $163 billion for the five years from 2024-25 to 2028-29, equivalent to 122 GW of potential new capacity. However, AEMO’s Draft 2026 ISP notes that currently only 24 GW of solar and wind projects will be operational by 2030 – that is, by 2030, renewable energy would contribute 75% of NEM supply, missing the 82% national renewable energy target.xxi While development is expected to catch up to help meet the 2035 emission targets, project delivery is constrained by planning approvals, the supply chain, gaining social license, and construction challenges.

Figure 4: Capacity, SWIS GW 2023 to 2042

Source: Government of Western Australia, 2023, SWIS Demand Assessment 2023 to 2042.

Storage for grid stability and energy reliability

Batteries, when paired with renewable energy, can store excess power during low-demand periods and release it during peak times. Their flexibility allows them to respond rapidly to demand, often within seconds. They can be deployed at various scales – from large grid-scale installations to smaller home systems. When aggregated, smaller batteries can form virtual power plants, enhancing grid stability.xxii

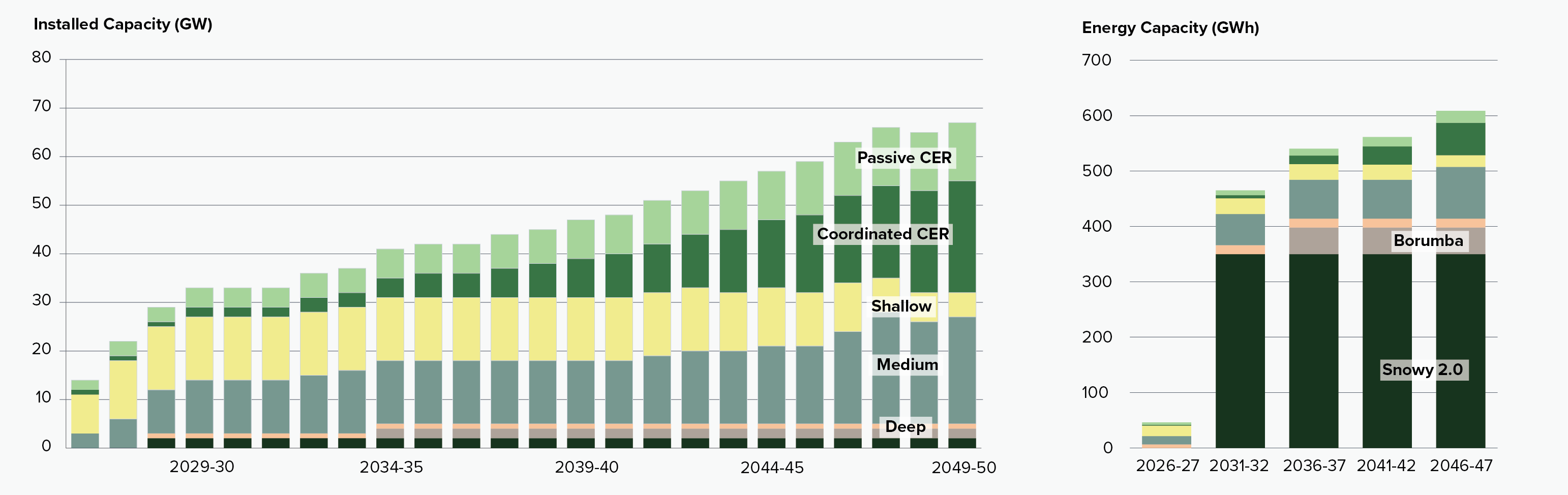

According to the Draft 2026 ISP, the NEM must expand its battery storage capacity from 3 GW to 33 GW by 2050 to meet net zero emissions targets. This includes 27 GW of grid-scale batteries and 6 GW of pumped hydro storage. Achieving this growth will require a diverse mix of storage technologies that can dispatch power over different timeframes (refer Table 22), including large-scale batteries, pumped hydro, and coordinated consumer energy resources (CER) such as home batteries and electric vehicles (EVs).

| Storage Type | Dispatchable power | Description |

|---|---|---|

| Consumer energy resources (CER) | 2 hours | Coordinated CER storage is managed as part of a virtual power plant, while passive CER storage is not. Includes rooftop solar, EVs, at-home batteries and community batteries. |

| Shallow | < 4 hours | Such as a utility-scale battery. |

| Medium | 4-12 hours | Grid-scale batteries or pumped hydro. These are vital for managing daily peaks, especially in the morning and evening. |

| Deep | > 12 hours | Needed for covering extended periods of low solar and wind output and for seasonal energy shifting. These systems are often supported by gas powered generation. |

As shown in Figure 5, while shallow storage, including passive and coordinated CER, will account for 60% of the NEM’s installed storage capacity (gigawatts) in the future, deep storage will underpin system reliability, accounting for between 70-80% of energy storage capacity (gigawatt hours) by 2030 and 2050. Energy storage capacity is the total amount of energy (gigawatt hours, GWh) a system can store and deliver over time.xxiii

Deep storage, including Snowy 2.0 (New South Wales) and Borumba (Queensland), will be needed for covering prolonged periods of ‘dark and still’ conditions associated with renewable lulls.

Queensland’s planned Borumba Pumped Hydro project is anticipated to add 48 GWh of storage capacity, while Snowy 2.0 would provide 350 GWh, which would be 1.3 and 9.5 times larger than all coordinated CER storage in 2050.

Such deep storage projects are critical. Currently, only three deep storage facilities – Temut 3 (New South Wales), Wivenhoe (Queensland), and Shoalhaven (New South Wales) – are operational, with Snowy 2.0 and Kidston Pumped Storage Hydro (Queensland), under construction.171

Figure 5: Storage installed capacity and energy storage capacity, NEM

Source: AEMO, 2026 Draft Integrated System Plan, figure 18

The Australian Government’s Capacity Investment Scheme offers incentives for large dispatchable storage, as does South Australia’s Firm Energy Reliability Mechanism, while New South Wales has a target of at least 16 GWh of storage by 2030.165 The Australian Government is also supporting the uptake of consumer batteries with its $7.2 billion Cheaper Home Batteries Program which subsidises household and small business battery systems.

Though many shallow and medium sized batteries will be delivered by the private sector, government investment may still be necessary to ensure grid stability and security through the availability of strategic medium and deep storage. Infrastructure Australia has previously listed National Electricity Market: dispatchable energy storage for firming capacity on the Infrastructure Priority List, which identified investments in dispatchable energy storage to support growing renewable energy generation.

The Australian Government is investing in storage projects through the Clean Energy Finance Corporation (CEFC) and Australian Renewable Energy Agency (ARENA), and directly, including:

- $8.48 billion in financing to Snowy Hydro, an Australian Government Business Enterprise, to deliver Snowy 2.0.xxiv

- $650 million in concessional finance, and $65 million in grant funding for Hydro Tasmania’s Tarraleah hydropower redevelopment, which will double the power station’s capacity from 90 megawatt (MW) to 190 MW with 20 hours of storage.172

Additional deep storage/pumped hydro projects are in planning, including:

- Cethana Pumped Hydro in Tasmania under the Battery of the Nation initiative, with approximately 14.5 GWh of storage.

- Mount Rawdon Pumped Hydro, a private project located south-west of Bundaberg in Queensland proposing up to 20 GWh of storage capacity.

- Capricornia Energy Hub Pumped Hydro, a proposed private generation facility in Queensland, with a storage capacity of 12 GWh.

- Phoenix Pumped Hydro, a proposed private facility in the Central-West Orana Renewable Energy Zone (New South Wales) with a storage capacity of around 12 GWh.

Major battery projects in Australia include the 3 GWh Supernode (Queensland) and Eraring (New South Wales) battery projects, both medium storage projects being delivered by the private sector.

Transmission projects, which are discussed further in the following section, are intended to help enhance the NEM’s access to these resources.

10-year national priorities

Australia has a range of renewable energy generation and storage needs to support the clean energy transition. Energy storage requirements range from short-duration to long-duration solutions.

In remote communities, renewable energy generation strengthens resilience, boosts local economies and supports better health outcomes. The 2026 Infrastructure Priority List includes the Northern Territory remote community power generation program proposal as a priority for future investment in the 2-4 year pipeline. Renewable energy generation can replace ageing diesel generators in 72 towns across the Northern Territory that supply electricity to remote and regional First Nations communities. This transition would lower operating costs and improve the resilience of energy infrastructure in remote communities often isolated during the wet season.

Batteries and deep storage are key to ensuring grid reliability and stability during periods of uncertain renewable supply. The 2026 Infrastructure Priority List includes the ACT renewable energy storage enhancement proposal as an immediate priority for planning to investigate Battery Energy Storage Systems in the Australian Capital Territory. Adding new firming capacity would help reduce the risk of power outages and rolling blackouts in the NEM, which can have detrimental impacts on network equipment, leading to potential security and reliability issues for those connected to the electricity grid.

_____

xix AEMO uses scenario planning to assess future investment needs in the energy system. Step Change Scenario reflects a pace of energy transition that supports Australia’s contribution to limit global temperature rise to less than 2°C.

xx Firming refers to maintaining the output from an intermittent power source for a required length of time.

xxi On average, solar and wind projects take four years from connection application to full output.

xxii A virtual power plant is a network of small, distributed energy resources (like solar batteries) that are linked and controlled using smart software.

xxiii Installed capacity (GW) is the maximum instantaneous power a plant can produce, while energy capacity (GWh) is the total energy produced over time.

xxiv This figure includes $1.38 billion equity injection in Budget 2019-20, and additional $7.1 billion financing (loan and equity) in Budget 2024-25.