Embodied Carbon Projections for Australian Infrastructure and Buildings

15 July 2024

Recommendations

This report offers the following six recommendations aimed at supporting the development of Australian Government decarbonisation policies for infrastructure and the built environment.

Report finding | Opportunities | Recommendations |

|---|---|---|

| The decarbonisation of the built environment suffers from industry silos and a lack of collective ambition. While governments and industry are working hard to manage their emissions, efforts often focus on individual assets, overlooking interconnected networks and systems. Moreover, project-level decarbonisation initiatives often commence late in the planning stages, risking the discretionary nature of carbon reduction goals and potential compromises through value engineering. | To decarbonise the built environment at scale, it is essential to take a comprehensive approach and work together across the value chain. This means seeing assets as part of a larger interconnected system, breaking down barriers across sectors, markets and jurisdictions and developing a unified strategy. By applying decarbonisation principles early on and considering the entire lifespan of buildings and infrastructure, it is possible to maximise opportunities to reduce embodied carbon and minimise trade-offs. | The Australian Government, working with state and territory governments, should develop a comprehensive national plan to actively promote the decarbonisation of emissions embodied in Australia’s built environment, in particular by:

|

| Limited understanding of decarbonisation and climate related issues across industry along with a lack of confidence in using lower carbon materials are obstacles to moving towards low carbon solutions. While individual projects may see success, there is a lack of collective data to support widespread adoption of innovative approaches. The Austroads Environment and Sustainability Taskforce, along with the Australian Government, state and territory governments, and New Zealand, are actively working together to fill knowledge gaps and promote new methods for reducing carbon in road-related infrastructure. At the same time, the Australian Government’s investment in the Infrastructure Net Zero Initiative aims to unite industry and government stakeholders to drive ongoing policy changes and innovation in cutting carbon emissions from infrastructure. | Decarbonisation at scale requires education and training for professionals, trades and consumers. Training should focus on addressing carbon literacy, specification of low-carbon products, and construction techniques with low-carbon materials. Sharing proven methods and project learnings can support broader knowledge uplift across industry. | The Australian Government, with state and territory governments should build carbon confidence and literacy for professionals, trades and consumers by:

|

Historically, Australia has lacked a nationally consistent way of measuring embodied carbon in the built environment. Different methods are used to calculate and claim carbon reductions and there is no single, trusted dataset for all construction material emissions factors. Without this, it is hard to access and compare the emissions of different products. Across Australia there is no uniform mandates to measure and report embodied carbon. Work is currently underway to develop standardised approaches. The National Australian Built Environment Rating System is developing an Embodied Carbon rating tool to enable new buildings and major refurbishments to measure, verify and compare their upfront embodied carbon. On 7 June 2024, Australian Infrastructure and Transport Ministers also approved the Embodied Carbon Measurement for Infrastructure: Technical Guidance, which provides a nationally consistent approach to measuring embodied emissions in infrastructure projects. However, further work is needed to implement consistent measurement, reporting, data collection and data assessment across Australia. | Decarbonisation should be based on a nationally accepted way of measuring embodied carbon, which is supported by a national database of emissions factors for construction materials to ensure consistency in measurement. Policy support for measuring and disclosing upfront carbon can help industry understand the true impact of new construction and stimulate the market for low carbon solutions. | The Australian Government, with state and territory governments, should continue developing a nationally standardised embodied carbon measurement system, which allows for consistent methods to collect, measure, and assess data about embodied carbon. This could involve:

|

A lack of consistent and continuous demand for low carbon products creates difficulties for the development of low carbon solutions that are commercially viable. Companies seeking to develop lower carbon products face cost premiums, and some domestic manufacturers have expressed concerns with carbon leakage from high-carbon, low-cost imports. The lack of valuation for carbon impacts in many projects results in cost-driven decision-making during procurement, often favouring low-cost options over initially specified low-carbon alternatives. In December 2023, the Infrastructure and Transport Ministers’ Meeting approved a nationally consistent set of carbon values for use in transport infrastructure projects. As of March 2024, Infrastructure Australia requires the use of these values in infrastructure proposal submissions. The Infrastructure Decarbonisation Working Group, led by the NSW Government and the Australian Government, is also developing policies to reduce embodied emissions in transport infrastructure. This includes the creation of a ‘carbon in procurement and contracts’ guideline to support the implementation of measures promoting transport decarbonisation. | A nationally agreed approach for stimulating demand for low carbon solutions would help to demonstrate consistency and reliability for the supply chain. Funding support for the development of low carbon materials will also help to speed up their adoption into Australia’s built environment. | The Australian Government, working with state and territory governments, should agree a common national approach to drive market demand for low carbon solutions. This could involve:

|

The unwillingness of the industry to embrace new project delivery approaches due to fear of risk exposure is impeding progress in decarbonisation The incremental effort involved in identifying risks associated with new delivery approaches and then allocating risk to the party best placed to manage is substantial, leading project teams to opt for traditional solutions and conservative procurement practices. | Asset owners and contractors need to share risks and rewards to encourage the adoption of lower-carbon solutions on projects. This could involve prioritising decarbonisation as a metric for project success, offering shared reward incentives through contracts, and developing new models for project delivery. Government funded projects that support trials and pilots of new solutions would provide data and insights to support investment decisions and increase industry confidence. | The Australian Government, working with state and territory governments, should develop new methods for project delivery which share risks and rewards for innovative approaches. This could involve:

|

| Supplier investment in low-carbon solutions is hampered by overly prescriptive product specifications on projects, which specify that materials must meet a certain prescriptive characteristic rather than performance outcomes. This inhibits the entry of new materials and solutions. Slow updates to industry standards and project specifications also mean that the pace of development will outstrip a standard or specification’s ability to keep up with the latest options available. | Governments and private entities should transition to performance-based specifications on projects, which focus on desired outcomes rather than specific product characteristics. This would allow for innovative approaches that deviate from traditional specifications and support the uptake of lower carbon solutions on projects. Faster, more agile processes should be introduced to ensure that standards and specifications can be updated in a timely way. | The Australian Government, with state and territory governments, should work with industry to drive national alignment on low-carbon expectations through performance-based standards and specifications. This could involve:

|

Foreword

It is with pleasure that I present this Embodied Carbon Projections for Australian Infrastructure and Buildings report, which, for the first time, uses our Market Capacity Program data to measure the embodied carbon intensity of forward-looking infrastructure and buildings pipelines across a five year period.

This report identifies that, in the near term, the biggest immediate opportunity for lowering embodied carbon emissions lies in upfront emissions from the manufacture and supply of materials. These easy-to-abate emissions represent almost 2% of the yearly national total, and are addressable via low-cost and practical decarbonisation strategies explored in this report.

In the long-term however, the decarbonisation of Australia relies on us cultivating the optimum conditions for success, today. This means developing an informed market that values carbon in policy, and consistently measures and reports embodied emissions.

To this effect, we have included six recommendations for governments to consider in the development of sectoral decarbonisation plans that will inform the Australian Government’s Net Zero 2050 plan and 2035 carbon reduction targets.

I would like to extend my thanks to the project team whose efforts culminated in this insightful research, and also express gratitude to all those involved across the jurisdictions and industry for their invaluable contribution which have enriched the depth and breadth of our findings.

Gabrielle Trainor AO

Interim Chief Commissioner

Executive summary

This Embodied Carbon Projections for Australian Infrastructure and Buildings report establishes a baseline for upfront embodied carbon in Australia’s built environment. It does this by estimating the carbon impact of the forward-looking construction pipeline for building and infrastructure from 2022–23 to 2026–27.

It finds that the built environment is directly responsible for nearly one third of Australia’s total emissions and contributes to over half of all emissions. Over the next five years, construction activity from the pipeline will be responsible for producing between 37 to 64 Mt CO2e per year. Almost a quarter of upfront emissions from construction activity over the next five years (or 2% of Australia’s total emissions in 2022–23 can be abated at no additional cost by employing practical decarbonisation strategies, such as material substitution. Targeted engagement with industry and government stakeholders indicated that this will require an informed market which values carbon in policy and consistently measures and reports embodied emissions.

The carbon impact of the forward looking construction pipeline is based on Infrastructure Australia’s National Infrastructure Project Database, which aggregates project level data for buildings, transport, and utilities projects valued over $100 million in New South Wales, Victoria, Queensland and Western Australia, and over $50 million in South Australia, the Australian Capital Territory, the Northern Territory and Tasmania, in addition to private building projects with a capital value of over $25 million. To account for the effect of project unknowns on construction material quantities and address gaps in smaller residential projects, an additional forecast of embodied carbon emissions was also conducted which aligns material demand quantities with estimates of national supply levels (See Section 5: Accounting for Uncertainty: Hybrid Analysis)

The report highlights key areas of opportunity for governments to consider in the development of sectoral decarbonisation plans that will inform the Australian Government’s Net Zero 2050 plan and 2035 carbon reduction targets.

Current embodied carbon initiatives

We note the following efforts of governments to lower embodied carbon in infrastructure and buildings:

The Australian Government

- Work is underway to develop nationally consistent frameworks for decarbonising infrastructure. Under the auspices of the Infrastructure and Transport Ministers’ Meeting, three workstreams were established to:

- develop a nationally consistent approach to measure embodied carbon for infrastructure, which will support industry action to reduce emissions and facilitate future benchmarking and target setting (led by Infrastructure NSW and approved in June 2024)

- develop a nationally consistent approach to valuing carbon for economic appraisal and policy evaluation (led by Infrastructure Australia and approved in June 2024)

- explore policy levers available to governments to reduce embodied emissions, including principles to support the identification of opportunities for the national harmonisation of policies to reduce embodied emissions, as well as inform governments’ selection of these policies (led by Transport for NSW with the Australian Government).

The National Australian Built Environment Rating System is developing a national framework for measuring, benchmarking and certifying emissions from construction and building materials. This will allow building owners to set robust and measurable targets for reducing embodied carbon in buildings.

State and territory governments

- NSW Government, through Infrastructure NSW, has published a Decarbonising Infrastructure Delivery Policy which sets expectations for NSW Government infrastructure delivery agencies on managing carbon in public infrastructure projects. This is supported by Measurement Guidance. In partnership with the Environment Protection Authority, Infrastructure NSW is also developing a monitoring framework to require infrastructure projects to report embodied carbon and maximise the use of recycled materials.

- Infrastructure Victoria has released advice on opportunities for the Victorian Government to reduce emissions of future public infrastructure investments. This advice focuses on policy and guidance to address emissions at all stages of development.

Section 1: Introduction

A report on embodied carbon in Australia’s infrastructure and buildings

This report offers a combination of quantitative and qualitative analysis to assist governments in understanding the potential for decarbonising infrastructure and buildings, as well as the increased usage of low embodied carbon materials in construction. These are key focus areas identified in the Australian Government’s most recent Infrastructure Policy Statement (November 2023).1

By presenting data and insights, it seeks to inform the development of policies aimed at reducing embodied carbon in the built environment. It also aims to initiate discussions on potential policy levers that align with this goal, such as the ongoing development of sector-specific plans by the Australian Government for the decarbonisation of buildings and transport infrastructure.

It responds to three pieces of legislation:

- The Climate Change Act 2022 (Cth), which legislates a 43% reduction in 2005 national greenhouse gas (GHG) emissions by 2030, and a net zero reduction by 2050.

- The Climate Change (Consequential Amendments) 2022 Act, which legislates for government institutions to focus on achieving emissions targets.

The Infrastructure Australia Act 2008 which requires Infrastructure Australia to consider the impact of infrastructure proposals on Australia’s net greenhouse gas emissions, the achievement of Australia’s GHG emissions reduction targets and any policy issues arising from climate change that Infrastructure Australia considers relevant to the proposal.

Baseline measures of carbon emissions for Australia’s infrastructure and buildings

This report leverages Infrastructure Australia data to analyse the embodied carbon emissions of Australia’s infrastructure and buildings pipeline. This includes estimating the embodied carbon that will be produced in the next five years if no action is taken, evaluating the potential emissions and costs associated with using low-carbon building materials and construction methods, and identifying barriers and government interventions that could increase the adoption of these solutions.

Section 2: Baseline Measures of Embodied Carbon presents baseline measures of carbon emissions produced by Australia’s infrastructure (listed below and depicted in Figure 1):

- Emission type (embodied, operational, enabled)

- Embodied emission type (upfront, use phase, end-of-life)

- Upfront carbon (materials manufacture, transport to site, construction process)

Also in Section 2: Baseline Measures of Embodied Carbon are the carbon and cost impacts of using like-for-like material substitutions in government infrastructure projects for two decarbonisation scenarios.

Projections based on forward-looking government construction pipelines

Embodied carbon projections in this report are based on the quantities of construction materials demanded by the forward-looking infrastructure pipelines of the Australian Government, and state and territory governments. These quantities have been determined using the analytical tools of Infrastructure Australia’s Market Capacity Program - an assumptions-based methodology that identifies market capacity risks by analysing infrastructure project data provided by governments, which, combined with private investment data provided by GlobalData, reflects around 75% of market demand in the forward estimates period.

Working towards Net Zero 2050

This report offers high-level recommendations for the Australian Government to work towards the reduction of embodied carbon from infrastructure and buildings in support of Net Zero 2050. These recommendations aim to initiate investigations and identification of policy levers that are best placed to achieve this objective, and were developed following extensive consultations with government stakeholders, industry members, and technical experts - see Appendix for a summary of our stakeholder consultation insights.

A summary of opportunities and recommendations is included in the Executive Summary of this report.

Embodied carbon policy: current state

Throughout Australia, governments are taking steps to design and implement policies targeting the reduction to embodied carbon in the built environment.

The Australian Government

The Australian Government is actively working to create consistent frameworks for decarbonising infrastructure and buildings. Three key workstreams were established under the auspices of the Infrastructure and Transport Ministers’ Meeting:2

- Measuring embodied carbon: Infrastructure NSW has developed a nationally consistent approach to measure embodied carbon in infrastructure. This will aid in reducing emissions, supporting industry action, and enabling benchmarking and target setting.

- Valuing carbon: Infrastructure Australia has developed a nationally consistent approach to valuing carbon for economic appraisal and policy evaluation.

- Policy levers and harmonisation: Transport for NSW, in collaboration with the Australian Government, is exploring policy levers to reduce embodied emissions. This includes developing principles to harmonize national policies aimed at reducing embodied emissions and guiding governments in policy selection.

The National Australian Built Environment Rating System is working on a national framework to measure, benchmark, and certify emissions from construction and building materials. This framework aims to help building owners establish measurable targets for reducing embodied carbon in buildings.

The Environmentally Sustainable Procurement Policy aims to improve the environmental sustainability of government procurements. The reduction in embodied carbon in construction projects is a key metric of the policy. As of July 2024, procurement of construction services over $7.5 million requires suppliers to measure and report on embodied carbon reduction.

State and territory governments

NSW Government, through Infrastructure NSW, has published a Decarbonising Infrastructure Delivery Policy which sets expectations for NSW Government infrastructure delivery agencies on managing carbon in public infrastructure projects. This is supported by Measurement Guidance. In partnership with the Environment Protection Authority, Infrastructure NSW is also developing a monitoring framework to require infrastructure projects to report embodied carbon and maximise the use of recycled materials

Infrastructure Victoria has released advice on opportunities for the Victorian Government to reduce emissions of future public infrastructure investments. This advice focuses on policy and guidance to address emissions at all stages of development.

Overview of the Market Capacity Program

This research is underpinned by Infrastructure Australia’s Market Capacity Program, a data-driven research initiative designed to help stakeholders understand the national infrastructure pipeline. By continuously monitoring market conditions and capacity to deliver infrastructure, the Market Capacity Program provides insights to inform government policies and management of infrastructure pipelines. The Market Capacity Program was set up in response to a request by Ministers at the Council of Australian Governments meeting of 13 March 2020.

The Market Capacity Program is underpinned by a National Infrastructure Project Database, a central database that brings together and organises project data. State and territory governments contribute to the database by providing regular, comprehensive, up-to-date information. A Market Capacity Intelligence System complements the database. This is an extensive set of analytical tools to examine and visualise capacity across different sectors, project types and resources. Together, this suite of tools, data and reports provide up-to-date evidence to better understand Australia’s infrastructure pipeline and the market’s capacity to deliver in the coming years.

Accounting for uncertainty

Given that Market Capacity Program analysis cannot account for future changes in cost, schedule, or scope, Section 5: Accounting for Uncertainty: Hybrid Analysis offers an alternate forecast of embodied carbon emissions, which considers the effect of project unknowns on construction material quantities - for example, resource shortages and typical project slippage. In addition, these alternative projections address gaps in smaller residential projects, expand material categories, and align calculated material demand quantities with estimates of national supply levels.

Section 2: Baseline measures of embodied carbon

Key findings

Embodied carbon from construction activity in 2023 contributed 10% of Australia’s total carbon emissions, with upfront carbon contributing 7%.

A steady reduction of upfront carbon is achievable by applying like for like decarbonisation strategies, with potential for 23% reduction on the baseline by 2027. This roughly equates to a reduction of 9 Mt CO₂e, or 2% of Australia’s national greenhouse gas (GHG) emissions in 2023.

The reduction of upfront carbon in the manufacturing of construction materials and the construction process provides a short-term opportunity for policymakers to consider in working towards Net Zero 2050.

To support decarbonisation policy design and implementation, this section provides baseline measures of embodied carbon in infrastructure, and estimated emissions and costs from the use of like for like material substitutions in government infrastructure.

Embodied carbon accounts for 10% of national emissions

Australian infrastructure and buildings were projected to contribute 57% of national carbon emissions in 2023. Of this, embodied carbon from construction activity in the built environment represents 10% of national emissions, as shown in Table 4.

Embodied carbon represents the sum of the GHG emissions associated with materials and construction processes throughout the whole lifecycle of an infrastructure or building asset, including material extraction, transportation, manufacturing, construction, use, replacement, demolition and end of life. These emissions are ‘locked in’ by the decisions made during the planning, design, procurement, delivery and maintenance of new construction projects.

As Australia strives towards net zero, it is crucial to address embodied carbon, which reflect the climate consequences of today’s construction decisions, and embed emissions for the lifetime of the asset.

Table 4: Breakdown of carbon emission projections for infrastructure and buildings, 2023

| Emission | Definition | 2023 emissions (kt CO2e) | Share of national emissions |

|---|---|---|---|

| Embodied | Emissions associated with materials and construction processes used over an asset’s life. | 54,400 | 10% |

| Operational | Emissions from asset use: mainly electricity and on-site combustion of diesel and natural gas. | 112,000 | 21% |

| Enabled | Emissions made possible by an asset’s existence, such as diesel emissions made possible by the presence of highways. | 137,000 | 26% |

The importance of addressing embodied carbon

While operational and enabled emissions represent a larger proportion of the total compared to embodied carbon, there are already many initiatives targeting them, and they can be reduced by decarbonising the electricity grid or using green hydrogen.

Embodied carbon is much harder to abate. While some embodied carbon will reduce as the grid decarbonises, others will not. This is because the carbon footprint of many building products (such as steel, cement, bitumen, glass, plasterboard, bricks and aggregates) comes from process heat and chemical emissions rather than from electricity.

As the grid decarbonises and progress is made on reducing the operational energy use of Australia’s buildings and infrastructure, embodied emissions are expected to account for a greater share of an asset’s carbon footprint over its lifecycle.

There is an opportunity for governments to increase their range of embodied carbon reduction policies as part of efforts to decarbonise the built environment, which have to date focused extensively on addressing operational emissions.

Focusing on upfront carbon

Embodied carbon can be divided into the different stages of an asset’s life at which they occur.

These include:

- Upfront embodied carbon emissions, which occur at the start of an asset’s life, up to practical completion. They include emissions from materials production, transport, construction waste and the construction process.

- Use phase embodied carbon emissions, which occur during an asset’s life when it is maintained, repaired, replaced and renovated. Examples include regular fitouts of buildings, recladding of buildings and maintaining/replacing road pavements.

- End of life embodied emissions, which occur at the end of an asset’s life. This includes emissions from deconstruction, demolition, transportation and waste management after the asset is no longer in use.

The analysis in this report focuses on upfront embodied carbon, defined here as the greenhouse gas emissions and removals associated with the creation of an asset, network or system up to practical completion.3

Figure 2 illustrates the activities underlying the infrastructure and buildings lifecycle modules as defined by international and European standards for lifecycle assessment of buildings and infrastructure assets.4,5,6,7,8

Activities factored into upfront carbon calculations include:

- Modules A1-A3: Manufacture of building products

- Module A4: Transport of building products to site.

- Module A5: Construction, which includes:

- land use change from land clearing

- construction waste

- construction energy

- commissioning energy.

Figure 2: Infrastructure and buildings lifecycle modules, highlighting upfront carbon

Based on data from Infrastructure Australia’s Market Capacity Program (2023), Australia’s construction pipeline is projected to produce between 37 Mt CO₂e and 64 Mt CO₂e of upfront carbon each year, between 2022–23 and 2026–27. Of this, buildings represent the largest share of the total upfront carbon, accounting for approximately half of total forecast emissions in most years. This is followed by utilities, which have the greatest variability, accounting for 14% of forecast upfront emissions in 2022–23 and 41% in 2026–27. Finally transport infrastructure accounts for approximately one-fifth to one-quarter of upfront emissions in most years. In 2023, upfront carbon from building activity is estimated to produce approximately 7% of Australia’s national emissions (see Table 5).

Table 5: Embodied carbon emission projections by lifecycle module, 2023

| Embodied carbon emissions | Definition | 2023 emissions (kt CO2e) | Share of national emissions |

|---|---|---|---|

| Upfront | Emissions from the creation of an asset, network, or system, up to the point of practical completion. | 35,200 | 6.6% |

| Use phase | Emissions from maintaining and/or refurbishing an asset. | 17,800 | 3.4% |

| End-of-life | Emissions from asset demolition and/or deconstruction. | 1,490 | 0.3% |

Materials manufacturing produces the most upfront carbon

Of the activities responsible for upfront carbon emissions, the manufacturing of construction materials (modules A1—A3 in Figure 2) account for most upfront carbon. These activities are described in Table 6.

Table 6: Upfront carbon projections for lifecycle modules A1—A3, A4 and A5, 2023

| Upfront carbon emissions | Description | 2023 emissions (kt CO2e) | Share of upfront carbon emissions from infrastructure and buildings |

|---|---|---|---|

| Materials manufacture (A1-A3) | Emissions from the manufacture of construction products, from extracting, harvesting, or recovering raw materials, through to the manufacturer’s outbound factory gate. | 27,500 | 75% |

| Transport to site (A4) | Transport of building products to site. | 1,680 | 5% |

| Construction (A5) | Emissions from asset construction including land use change/clearing, waste, and energy (including commissioning). | 7,400 | 20% |

Across all sectors, materials manufacturing dominates upfront carbon emissions

Materials manufacturing (modules A1—A3 in Figure 2) represents the highest proportion of upfront carbon emissions across all sectors. This can be seen in Figure 3, which shows a breakdown of emissions by lifecycle module for 2023–24.

Figure 3: Upfront carbon projections for lifecycle modules A1—A3, A4 and A5 by sector, FY 2023–24

The dominance of materials manufacturing in upfront carbon is most pronounced in the buildings sector in terms of volume (21 Mt CO₂e) and in the utilities sector in terms of share (89%). Construction is the second most significant lifecycle stage, accounting for 9% to 28% of total emissions. The key contributors to construction emissions vary between asset types. Some are due to construction or commissioning energy, while others are the result of land use change. Transport of building products to site is the least significant lifecycle module relatively, accounting for only 2–5% of total emissions.

Emissions broadly follow population, but priorities differ between regions

Carbon emissions shown in Figure 4 reflect the five-year infrastructure ambitions of each state and territory. The largest share of emissions is forecast to come from New South Wales, followed by Victoria, Queensland, Western Australia, South Australia, Tasmania, the Australian Capital Territory and the Northern Territory. While these emissions broadly follow differences in population, there are major differences in how they are made up. South Australia, Queensland and New South Wales plan to invest heavily in utilities, particularly utility solar. Tasmania, Western Australia and Victoria plan to invest in transport infrastructure. The Australian Capital Territory and the Northern Territory are focused on buildings.

Figure 4: Upfront carbon emissions of states and territories, FY 2024

The potential for low-carbon building materials and construction methods

This research also investigated the carbon and cost impact of using like-for-like, decarbonisation strategies in forthcoming public infrastructure projects found in Infrastructure Australia’s Market Capacity Program database.

The adoption rates for decarbonisation strategies were calculated under two scenarios, reflecting a mid-level and maximum rate of adoption The Maximum Decarbonisation Scenario represents the highest level of ambition that industry stakeholders felt were achievable by 2026–27, assuming that cost was not a barrier. The Mid-level Decarbonisation Scenario uses lower uptake rates and reduces the use of decarbonisation strategies that are particularly expensive.

Table 7 presents a summary of the different uptake rates per scenario. Section 4: Cost and Carbon Abatement Potential examines cost and carbon abatement potential of each strategy.

Table 7: Uptake rates per decarbonisation scenario

| Decarbonisation strategy | Baseline* | Mid-Level Decarbonisation by 2026–27* | Maximum Decarbonisation by 2026–27* |

|---|---|---|---|

| Supplementary cementitious materials replace cement | 0–35% | 40% | 50% |

Reclaimed asphalt pavement replaces asphalt in:

| 0–10% | 0–25% |

|

Recycled crushed concrete replaces aggregates in:

| 0–5% 0% | 5–20% | 10–30% |

| Structural steel lightweighting | 0% | 50% | 100% |

| Reinforcing steel lightweighting | 0% | 50% | 100% |

| Fibre reinforcing replaces mesh/bar | 30% | 60% | 100% |

| Steel made in electric arc furnace with 100% renewable electricity | Grid average | 50% | 100% |

| Hydrated lime replaced in asphalt | 0% | 100% | 100% |

| Aluminium made with 100% renewable electricity | Grid average | 25% | 50% |

| Biodiesel in construction | 5% | 10% | 20% |

| Renewable electricity in construction | Grid average | 30% | 100% |

* A range indicates that uptake rates vary by state and typecast.

23% of upfront carbon from public infrastructure could be abated by 2026–27

Our analysis concludes that under the Maximum Decarbonisation Scenario, the upfront carbon emissions from public infrastructure could be 23% lower in 2026–27 with the use of like-for-like decarbonisation strategies considered in this report – see Table 8.

Table 8: Carbon impact from Maximum Decarbonisation Scenario and reduction against Baseline Scenario

2022–23 | 2023–24 | 2024–25 | 2025–26 | 2026–27 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

kt CO₂e | Change | kt CO₂e | Change | kt CO₂e | Change | kt CO₂e | Change | kt CO₂e | Change | |

| Buildings | 21,000 | 0% | 27,000 | -5% | 30,000 | -9% | 21,000 | -19% | 9,900 | -31% |

| Transport | 9,800 | 0% | 11,000 | -4% | 10,000 | -7% | 8,300 | -16% | 6,900 | -25% |

| Utilities | 5,300 | 0% | 13,000 | -2% | 19,000 | -4% | 15,000 | -8% | 14,000 | -16% |

| Total | 37,000 | 0% | 52,000 | -4% | 59,000 | -7% | 45,000 | -15% | 30,000 | -23% |

A 23% reduction in upfront carbon emissions from public infrastructure is equivalent to a reduction of 9 Mt CO₂e, roughly 2% of Australia’s gross national greenhouse gas emissions of 529 Mt CO₂e in FY 2023.9

This scenario would lead to a cost saving of $160 million (see Table 9), which is equal to 0.14% of the total value in Infrastructure Australia’s Market Capacity Program pipeline.

Table 9: Carbon and cost changes for the three decarbonisation scenarios in 2026–27

| Scenario | Carbon abatement | Cost |

|---|---|---|

| Baseline | No change | No change |

| Mid-level decarbonisation | 13% reduction | 0.24% cost saving |

| Maximum decarbonisation | 23% reduction | 0.14% cost saving |

A breakdown of the costs of the Maximum Decarbonisation Scenario is shown in Table 10. Replacing materials with lower-carbon alternatives results in an overall saving in material spend as cost-saving strategies more than compensate for those with a cost uplift. Increases in construction and commissioning costs are due to the use of biodiesel and renewable electricity. The increase in labour cost is due to an estimated increase in structural engineering fees to optimise structural steel (i.e., to reduce the amount of structural steel needed to achieve the desired level of performance).

Table 10: Cost impact from the like-for-like use of replacement materials, by input (Maximum Decarbonisation Scenario)

| Cost | Original cost ($million) | Additional cost ($million) | Change |

|---|---|---|---|

| Materials | $36,000 | $-690 | -1.9% |

| Construction | $8,300 | $240 | 2.9% |

| Commissioning | $680 | $85 | 13% |

| Labour | $45,000 | $200 | 0.44% |

| Unaffected | $26,000 | $0 | 0% |

| Total costs | $116,000 |

| 0.14% |

Under the Mid-level Decarbonisation Scenario, a 13% reduction in upfront carbon emissions is achievable with a larger cost saving of $280 million – or 0.24% of the total project value in Infrastructure Australia’s Market Capacity Program pipeline.

These scenarios show the significant potential for replacement materials in lowering embodied carbon emissions in infrastructure. However, it is worth noting that emission projections may not be realised exactly as presented as they are subject to government ambitions, market conditions, and emissions that occur beyond Australia’s territorial boundaries, which that may or may not change over time.

While a 23% saving in upfront carbon would be a significant contribution to Australia’s decarbonisation agenda, eliminating the other three quarters of upfront carbon emissions from the construction pipeline will need a different approach. It will need building products to be decarbonised from the supply side, and changes in how Australia plans, designs and procures assets so that embodied carbon is considered early. The only way to effectively reduce embodied carbon at scale is to start early and coordinate through the value chain.

Section 3: Barriers and opportunities

A conscious and concerted national effort is going to be crucial in meeting Australia’s net zero commitments. Successful decarbonisation of the built environment will require coordinating across the whole infrastructure planning, delivery and operation system, and a step change in how infrastructure and building assets are planned, built, operated, maintained and reviewed. This also involves overcoming a series of obstacles to change.

Taking insights from our consultation with industry and government stakeholders, this section explores obstacles to reducing embodied carbon in the built environment and provides recommendations for the Australian Government as it designs and implements targeted decarbonisation policies.

RECOMMENDATION 1

The Australian Government, working with state and territory governments, should develop a comprehensive national plan to actively promote the decarbonisation of emissions embodied in Australia’s built environment, in particular by:

- linking new construction decisions to Net Zero 2050 and 2035 reduction targets

- using the decarbonisation hierarchy to drive a clear strategy for reducing whole-life carbon from a project’s ‘needs’ stage to lock in the greatest opportunity to influence carbon reductions

Using lifecycle thinking to manage environmental and social impacts, minimise carbon footprints and avoid trade-offs

Disjointed operating environments are not conducive for achieving net zero targets

The individual carbon-reduction efforts of governments are a welcome first step on the path to national decarbonisation.

While many individual initiatives are underway, there is no overarching plan for targeting embodied carbon in the built environment. This limits the scope for collaboration across the built environment and linking new construction with Australia’s ambition for a net zero transition.

At the individual asset level, decarbonising a building or infrastructure asset is often considered without studying the implications for carbon on the wider system that the asset belongs to. Disconnected operations or any form of tunnel vision in decision making is a barrier to just transition, and can result in unforeseen trade-offs or unintended social, environment and/or economic impacts.

To address this, decarbonisation of the built environment should be addressed using a systems-based approach and through close collaboration across the value chain.

Using lifecycle thinking, which considers the impacts that asset owners and managers can control and influence when assets are created, operated and used ensures that multiple environmental and social impacts are considered across an asset’s whole lifespan.

Asset owners should also collaborate with other members of the value chain to speed up decarbonisation through the project delivery process. Early engagement and collaboration among value chain members such as owners and managers, designers, constructors, procurers and product/material suppliers is needed at all levels, from system to asset in order to effectively reduce carbon emissions.

Applying the decarbonisation hierarchy

To maximise whole-life carbon reduction and scale up the individual efforts of individual project teams, stakeholders should use the decarbonisation hierarchy (see Figure 5) to evaluate need, assess alternatives, adopt low carbon solutions, and improve. The greatest opportunity to avoid or reduce emissions occurs at the ’need’ stage, and gradually decreases through the design, materials selection, construction, and operation stages. Whole-life carbon can be influenced again at the end of an asset’s first life, if/when it can be refurbished, repurposed, deconstructed and/or decommissioned.

Figure 5: The decarbonisation hierarchy adopted from PAS 2080 (2023)

RECOMMENDATION 2

The Australian Government, with state and territory governments, should build carbon confidence and literacy in buildings and infrastructure by:

- complementing the ongoing efforts of the Austroads Environment and Sustainability Taskforce and the Infrastructure Net Zero Initiative to develop education programs for professionals, trades and consumers which target carbon literacy and low carbon product specifications and construction

- developing a national sharing platform for industry practitioners to showcase learnings from projects, pilots, concessions, model contracts and specifications for low carbon solutions

Piloting projects to trial new solutions and produce data about new products and construction techniques.

Widespread climate illiteracy and a lack of knowledge sharing can delay uptake of lower carbon materials

Australia’s decarbonisation efforts are detrimentally impacted by a general lack of understanding among industry professionals, trades, and consumers of climate and carbon issues (climate literacy), myths concerning low carbon materials and an absence of detailed and actionable learnings.

As assets are built or renewed, product choices are made based on current knowledge and perceptions developed over time. Myths about the difficulties and impracticality of using lower-carbon materials are common, and influence project decisions at both design and procurement stages. Where the availability, quality and performance of low-carbon construction materials are not well understood, hesitancy in their adoption is to be expected.

Knowledge about characteristics of low carbon products needs to be supplemented with practical awareness and know-how on their use for a project. Lack of confidence about specification and use results in low and fragmented demand for low-carbon products, which slows supply chain development due to insufficient demand, and less product availability.

Use of low-carbon products on projects often rely on substantial trials and testing, which are essential to ensure that alternative products are fit for purpose for their intended applications. Without evidence of multiple prior successes, project teams may be unwilling to use lower carbon alternatives which is problematic as test results are rarely published and case studies lack the detail required to replicate results.

One example of efforts to address these gaps in the industry and promote innovative building techniques in the transport infrastructure sector can be seen in the Austroads Environment and Sustainability Taskforce, comprising the Australian Government, state and territory governments, and New Zealand Government. Together, they are developing guidance, conducting research, and updating Austroads standards.

Additionally, the Australian Government has invested in the Infrastructure Net Zero Initiative, which brings together industry and government stakeholders to achieve the shared goal of decarbonising infrastructure. This collaboration recognises the shared responsibility of decarbonisation and the opportunity to create an aligned and effective use of collective time, resources, and expertise to accelerate the highest-priority initiatives to drive lasting policy change and industry innovation.

RECOMMENDATION 3

The Australian Government, with state and territory governments, should continue developing a nationally standardised embodied carbon measurement system, which allows for consistent methods to collect, measure and assess data about embodied carbon.

This could involve:

- Establishing a national database of default emissions factors and EPDs to support embodied carbon measurement, and be a single source of truth for practitioners in the built environment.

- Setting requirements to measure and disclose upfront carbon on projects over a threshold value and make use of collected data for setting best practice targets informed by benchmarks for different asset classes.

- Investigating ways to drive national alignment on data to support carbon calculations, including standardising the collection of construction and commissioning data.

Standard measures and tools are needed for meaningful progress

Reducing carbon emissions at scale is only possible with reliable and consistent measurement tools. Implementing a standard methodology and data system at national level poses a significant challenge.

Historically, Australia has lacked a nationally consistent way of measuring embodied carbon in the built environment. Various methods are used to calculated and claim carbon reductions on projects, leading to a lack of consistency and credibility in measurement, with inconsistent and non-comparable results. This makes it difficult for stakeholders to accurately calculate and track carbon emissions. Additionally, there is no comprehensive dataset for process-based lifecycle analysis emissions factors, which makes it difficult to access and compare the emissions of different building products. Furthermore, a shortage of compliant product data, such as third party verified EPDs, which limits the ability for decision makers to make informed low carbon choices when selecting building materials.

Recognising the imperative to consistently measure, compare and set reduction targets for embodied carbon in buildings, the National Australian Built Environment Rating System (NABERS) is working to create an embodied carbon rating tool for buildings, which would allow building owners to set robust and measurable targets for reducing embodied carbon in buildings. In concurrence, the Infrastructure and Transport Ministers’ Meeting has approved the Embodied Carbon Measurement for Infrastructure: Technical Guidance, a nationally consistent approach to measuring embodied emissions in infrastructure projects.11 Further work will involve developing and maintaining a national emissions factor library and nationally consistent data reporting and collection.

RECOMMENDATION 4

The Australian Government, working with state and territory governments, should agree a common national approach to drive market demand for low carbon solutions.

This could involve:

- developing nationally consistent procurement guidance through the Infrastructure Decarbonisation Working Group focused on enabling low carbon solutions in project requirements

- addressing cross-border carbon leakage and ensuring a means of fair carbon accounting between domestic and imported products, through the Australian Government’s ongoing work to investigate a domestic Carbon Border Adjustment Mechanism

- exploring funding or grants models to reduce the cost burden for projects to adopt lower carbon products and technologies

- investing in sustainable finance instruments to incentivise the adoption of low carbon materials and technologies on projects, by working with concessional finance providers

- investigating incentives for low carbon construction with planning authorities.

Industry needs a steadier flow of demand to justify decarbonisation investment

Industry is less willing to create more products and solutions that have low carbon impact, because the demand for them is not dependable. This hinders the advancement of the sector and the country as a whole.

Stakeholders identify several causes of demand dependability:

- The lack of common targets or incentives to drive demand for lower carbon solutions across jurisdictions.

- A focus on upfront cost that leads to low-carbon products being descoped in favour of lower-cost yet higher-carbon alternatives. A contributing factor is that carbon is not currently valued in the decision-making process for many projects.

- Suppliers not being engaged early enough in the project, limiting their ability to provide innovative solutions that meet design requirements as well a lower-carbon alternative. Once designs are finalised, the options for low carbon products become more limited.

- The high cost of product trials that reduce the pool of projects willing to undertake them.

- Leakage of carbon into Australia through higher-carbon, low-cost imports, which deters local, low carbon product development.

Many stakeholders interviewed for this report called for fairer carbon accounting, including the Building Products Industry Council and representatives of the steel industry, for who carbon leakage was regarded as an item of importance for government intervention.

In March 2023, the Australian Government announced it would undertake a review of carbon leakage as part of the Safeguard Mechanism reforms. The review will assess carbon leakage risks and policy options to address them, including the feasibility of an Australian Carbon Border Adjustment Mechanism. The review will focus on trade-exposed goods under the Safeguard Mechanism, particularly steel and cement which are key inputs for many types of infrastructure. The review’s first consultation paper was released on 13 November 2023 and closed on 12 December 2023. A second round of consultation will be undertaken in mid-2024. This review is expected to be completed by 30 September 2024.

The delivery of major infrastructure projects presents a unique opportunity for the Australian Government to drive decarbonisation outcomes. For instance, the Infrastructure Policy Statement, released in November 2023 notes that as emissions reduction techniques emerge, the Australian Government expects them to be factored into project delivery. This lays a clear foundation on which project selection funding decisions could be made in future.

There is also work underway to drive a more consistent approach to procurement. Through the ITMM, the Infrastructure and Transport Ministers’ Meeting, the Infrastructure Decarbonisation Working Group, chaired by NSW and the Commonwealth, is developing a ‘carbon in procurement and contracts’ guideline to inform the implementation of measures to ensure transport infrastructure projects support decarbonisation goals.

To elevate the consideration of carbon in project decision making, ITMM approved a nationally consistent set of values for use in transport infrastructure projects. Infrastructure Australia has introduced a requirement that infrastructure proposals submitted to Infrastructure Australia must use the nationally consistent set of carbon values in their submissions from July 2024.

RECOMMENDATION 5

The Australian Government, working with state and territory governments, should develop new methods for project delivery which share risks and rewards for innovative approaches.

This could involve:

- specifying outcomes and expectations of project delivery that embeds specific requirements for decarbonisation

- developing performance based, collaborative contract models and business cases, which assume the use of low carbon materials, early contractor involvement on projects, embodied carbon analysis in pre-tender processes, and clear direction for decarbonisation in tender documentation

- exploring opportunities to include trials of new materials in flagship projects and sharing learnings.

Industry confidence to invest in decarbonisation is low, for fears that risks may not be rewarded

Stakeholders identified fear of risk exposure as one of the major barriers hindering effective decarbonisation efforts. This reluctance stems from industry inertia, where trying new approaches or technologies to reduce carbon emissions is often seen as risky. Hesitance is further compounded by industry’s limited bandwidth, as it contends

with numerous commercial and workforce challenges alongside the complexity of the bidding process. Government procurement practices were reported to be conservative, undermining the imperative to tackle climate change and adopt progressive policies.

This inherent reluctance to take risks has also led to a resistance to pilot new projects as well as a preference to pass on risks to other parties. This is particularly evident in traditional contract models, where risk is typically shifted to the constructor in post-tender D&C (design and construct) contracts. Unfortunately, by this stage, the opportunity for significant decarbonisation in the project has often passed, leaving the constructor with limited options for reducing carbon.

Moreover, the aversion to risk has also hindered the willingness to try new and innovative approaches. Many stakeholders reported that there is a preference for familiar and low-risk solutions, instead of considering effective or innovative alternatives. As a result, even when new and well-tested solutions are available in other countries, there is a reluctance to adopt them in Australian projects. This is exemplified by the use of general purpose limestone cement, which is commonly

used overseas by not yet embraced in Australia. Overall, the apprehension towards risk and change in the industry is seen as a barrier to decarbonisation efforts.

RECOMMENDATION 6

The Australian Government, with state and territory governments, should work with industry to drive greater national alignment on low-carbon expectations through performance-based standards and specifications.

This could involve:

- establishing unified specifications and guidelines that promote the adoption of lower-carbon products more consistently across all jurisdictions. This should be incorporated into widely accessible model specification clauses to enable standardised practices

- procuring using performance-based specifications, that allow for materials and solutions to be judged on meeting performance criteria, rather than specifying that they must be of a certain characteristic.

Leading efforts to expedite the updating of standards and specifications, developing a more efficient system and providing funding for critical updates to keep pace with evolving options.

Product development is hindered by traditional standards and specifications

During consultation, industry stakeholders were frustrated by existing specifications, which prescribed specific characteristics for products rather than performance outcomes. This can limit the entry of new and innovative materials into the market.

Existing construction bias and out-dated material standards and specifications often preclude the use of lower-carbon materials, mixes and processes. Traditionally, specifications prescribe characteristics of a compliant product, such as a minimum required composition. These are typically narrow, focusing on known solutions.

Another barrier to progress is fragmentation in product specifications across jurisdictions, which discourages investment by diluting market demand. This is further compounded by Australia’s inherent challenges of low population and geographical spread, making it difficult to justify product changes due to inconsistent demand for specific requirements.

The low pace of updates to standards and specifications is another significant barrier. Stakeholders expressed frustration at the lag in updating these standards, which makes it difficult for the industry to keep up with the latest low carbon materials. According to some stakeholders, slow progress in the update of existing stipulations mean that new solutions are judged on their adherence to narrow and prescriptive specifications rather than their performance.

As innovation in low carbon materials continues to advance, it is imperative that measures are taken to speed up the process of updating standards and specifications.

To overcome these barriers, it is necessary to address the issue of consistency in product specifications at a national level. There is also a need to transition to performance-based specifications and ensure that standards and industry specifications are updated in a timely manner.

Section 4: Cost and abatement potential

Analysis presented in Section 2: Baseline Measures of Embodied Carbon showed that Australia can reduce upfront carbon emissions from its pipeline of infrastructure and buildings by up to 23% in 2026–27 by applying like-for-like decarbonisation strategies considered in this report.

The cost and carbon abatement potential of each decarbonisation strategy is shown in Figure 6. Four of the 11 groups of strategies considered in this report lead to a cost saving at the project level – recycled crushed concrete replaces aggregates in concrete and pavement sub-base; reclaimed asphalt pavement replaces asphalt in base course and wearing course; structural steel lightweighting and hydrated lime replaced in asphalt - and one is cost neutral – reinforcing steel lightweighting. The following remaining strategies incur a cost, shown in red, however most costs are small compared to the value of assets in the pipeline:

- Aluminium made with 100% renewable electricity.

- Steel made in an electric arc furnace with 100% renewable electricity.

- Supplementary cementitious materials that replace cement.

- Renewable electricity in construction.

- Steel fibre reinforcing that replaces steel mesh/bar reinforcing.

- Biodiesel in construction.

Of the strategies, biodiesel uptake is by far the most expensive, with relatively small benefit to reducing greenhouse gas (GHG) emissions. The Maximum Decarbonisation Scenario assumes that usage increases from 1% in 2022–23 to 20% by 2026–27 (i.e., nationwide adoption of a B20 blend across the construction sector. However, with current pricing, this strategy becomes expensive at the national level. As such, the Mid-Level Decarbonisation Strategy assumes a moderate uptake of biodiesel beyond current levels.

The strategies with the greatest influence on upfront carbon are:

- steel made from electric arc furnace with 100% renewable electricity

- reinforcing steel lightweighting

- structural steeling lightweighting

- supplementary cementitious materials replace cement

- renewable electricity in construction and commissioning.

Figure 6: Marginal abatement cost curve, 2026–27

Section 5: Accounting for uncertainty: hybrid analysis

The analysis in this report is based on Infrastructure Australia’s Market Capacity Project Database. This system aggregates project-level data to create a comprehensive overview of Australia’s infrastructure and building investment pipeline. This data is informed by budget processes and forward projections derived from budget estimate periods.

However, the landscape for project delivery has become progressively challenging, with constraints of available skilled labour and resources, market fluctuations, and inconsistencies in project and portfolio planning standards. Consequently, delays due to slippage are now widespread, which can lead to over-estimation of material demand.

Further, Infrastructure Australia’s Market Capacity project database focuses on major projects per state.

Major projects are defined as:

- infrastructure projects with a capital value of $100 million or more in New South Wales, Victoria, Queensland, and Western Australia

- infrastructure projects with a capital value of $50 million or more in South Australia, Tasmania, the Australian Capital Territory, and theNorthern Territory

- private building projects with a capital value of $25 million or more

- all energy projects, regardless of capital value.

The forecast may overestimate spend - and therefore upfront carbon - in some areas as a result of project slippage and threshold values, while underestimating it in others.

This project applies two scenarios to manage uncertainty:

- Pipeline Analysis: Calculations are based solely on the pipeline of infrastructure and building projects from Infrastructure Australia’s National Infrastructure Project Database, without any scaling. Projects below the thresholds above are excluded. Projects are reported in the year they are forecast, without accounting for potential slippage. In practice, this means that most of the residential housing market is excluded and that the pipeline is too full, particularly for the next 2—3 years (meaning it cannot all be delivered within the planned time horizon).

- Hybrid Analysis: This analysis is designed to achieve a more realistic forecast of future embodied emissions, and represents a more comprehensive dataset for buildings. This is done in four steps:

- Fill gaps for buildings under $25 million

Data from the Australian Bureau of Statistics (ABS) is used to account for construction of all buildings, regardless of their capital value.12,13 Forecasts from Master Builders Australia were used to project the ABS data into the future.14 - Expand the material categories for buildings

Additional materials (e.g., aluminium, glass and building services) is added to Infrastructure Australia’s materials classification to capture more embodied emissions from buildings. - Account for project slippag

Historic building approvals data from Australian Bureau of Statistics was used to account for project slippage and project cancellations. Construction rates for transport and utilities were not adjusted. - Reconcile quantities of calculated material with the market’s ability to supply these materials

Material quantities were summed to determine the deviation from total material supply at the national level. These comparisons were only made for a small number of materials where data was available or could be calculated, namely asphalt, total cementitious materials, reinforcing steel and structural steel. Where there were significant deviations (>±10%), project volumes were scaled to match total material demand. A rate of 5% year-on-year growth was allowed for per material category. (The reason for applying slippage factors first was to try to get a better balance across the project types before scaling up/down.)

Hybrid analysis findings

Upfront carbon emissions from construction activity in Australia’s buildings and infrastructure under the Hybrid analysis was calculated as 38 Mt CO₂e in 2022–23, the baseline for this study. This is equivalent to 7% of Australia’s total greenhouse gas (GHG) emissions in 2022–23. Use phase embodied carbon was estimated to be 18 Mt CO₂e, and end-of-life embodied carbon was estimated to be 1.5 Mt CO₂e (Table 11).

For detailed results of the hybrid analysis please refer to the report Supporting Appendices: Embodied Carbon Projections for Australian Infrastructure and Buildings.

Table 11: Embodied carbon emissions by lifecycle module, hybrid analysis (2022–23).

| Embodied carbon emissions | Definition | Emissions | Share of national emissions |

|---|---|---|---|

| Upfront | Emissions from the creation of an asset, network, or system, up to the point of practical completion | 38,200 | 7.2% |

| Use phase | Emissions from maintaining and/or refurbishing an asset | 17,800 | 3.4% |

| End-of-life | Emissions from asset demolition and/or deconstruction | 1,480 | 0.3% |

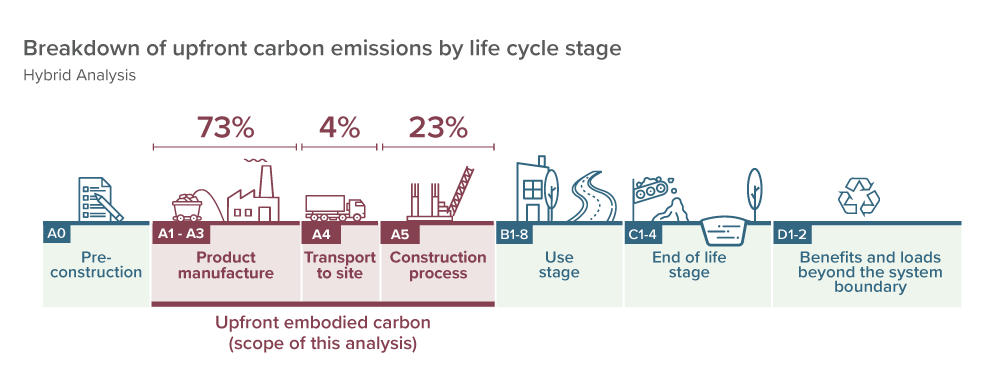

Most upfront carbon emission come from manufacturing construction products. Figure 7 provides a breakdown of upfront carbon emissions by lifecycle module. Construction products make up 73% of upfront emissions (modules A1 to A3 in carbon footprint standards). The remaining 27% comes from transport (module A4, 4%) and construction (module A5, 23%). In the construction phase, emissions come from four main sources: land use change for greenfield sites, construction waste, construction machinery and commissioning.

Figure 7: Breakdown of upfront carbon emissions by lifecycle stage using the hybrid method

Figure 8 presents a 5-year view of upfront carbon emissions from the infrastructure and buildings construction pipeline. Under the hybrid analysis, the upfront embodied carbon in Australia’s pipeline of infrastructure and buildings is forecast to be between 40 Mt CO₂e and 56 Mt CO₂e each year for the next 5 years, equating to 256 Mt CO₂e. Buildings represent the largest share, accounting for approximately half of the total forecast carbon emission (133 Mt CO₂e). This is followed by Utilities, which accounts for approximately 28% of the total emissions (71 Mt CO₂e). Transport infrastructure accounts for approximately a fifth of the total (52 Mt CO₂e).

Figure 8: National emissions over 5 years (hybrid analysis).

Figure 9 presents forecast upfront carbon using both the hybrid analysis (lighter filled stacked bars) and the pipeline analysis (darker filled stacked bars). The pipeline analysis shows dramatic growth in upfront carbon (high ambition in the short-term) and then decline (projects later in the time horizon not yet identified and committed). The hybrid analysis attempts to correct for this variability and therefore shows steady growth over the 5-year period between 2022–23 and 2026–27. It shows a steady increase until FY 2025, followed by a levelling out in 2025–26 and 2026–27.

Comparing the two analyses:

The total results are similar for the years 2022–23 to 2025–26. However, the make-up of these results is quite different. For buildings, the pipeline analysis is skewed towards larger projects, many of which will not be built in the forecast year. The hybrid analysis is influenced by many smaller projects, particularly residential building construction.

The pipeline analysis shows a rapid rise in construction, followed by a decline. The hybrid analysis is more stable over time. This is due to the difference in underlying approach for forecasting building construction, in which the pipeline analysis relies on self-reporting, and the hybrid analysis forecasts future building construction activity based on past construction activity.

Figure 9: A comparison of national emissions over five years using the hybrid analysis and pipeline analysis

Figure 10 shows a breakdown of the emissions by project type using the hybrid analysis for 2022–23. Detached residential buildings, multi-unit residential buildings and utility solar are forecast to have the highest upfront carbon footprint at the national level, with detached residential buildings in first place, due to the sheer number constructed. The next group of project types is state roads (Freeway/Highway), warehouse and office buildings – with state roads and warehouses having a relatively similar forecast upfront carbon footprint in 2022–23. Wind utilities, semi-detached residential buildings, retail stores and railway stations round out the top 10.

Figure 10: Embodied carbon for the 10 highest contributing typecasts in baseline year 2022–23 (hybrid analysis)

Figure 11 shows the carbon and cost changes for both the hybrid and pipeline Analysis, under the Mid-Level Decarbonisation Scenario and Maximum Decarbonisation Scenario. According to the hybrid analysis, the Maximum Decarbonisation Scenario is able to achieve a 21% carbon reduction on the pipeline by 2026–27, with a cost uplift of $37 million. The more moderate Mid-Level Decarbonisation Scenario can achieve a 12% carbon reduction on the pipeline for a saving of $200 million.

Figure 11: Carbon and cost changes from decarbonisation scenarios in FY 2027

| Scenario | Carbon abatement | Cost | ||

|---|---|---|---|---|

Pipeline | Hybrid | Pipeline | Hybrid | |

| Mid-Level Decarbonisation | 13% reduction | 12% reduction | 0.24% saving | 0.08% saving |

| Maximum Decarbonisation | 23% reduction | 21% reduction | 0.14% saving | 0.02% uplift |

Section 6: Methodology and Assumptions

Methodology overview

This report calculates:

- A baseline carbon footprint for infrastructure and buildings. The baseline carbon footprint represents the upfront carbon that is expected to result from Australia’s construction pipeline of buildings and infrastructure between the financial years 2022–23 and 2026–27, if no action is taken. It assumes that the adoption of low-carbon technologies remains at 2022–23 levels.

- The potential to reduce this baseline carbon footprint by substituting materials and energy with low-carbon alternatives, under two decarbonisation scenarios. Two decarbonisation scenarios are used to represent two technically achievable, levels of ambition for uptake of decarbonisation strategies.

- The mid-level decarbonisation scenario includes low-carbon technologies that are available on the market today, have proven technological viability, are cost competitive, and can be scaled up to the national level by 2026–27.

- The maximum decarbonisation scenario is designed to be an achievable best case. It assumes that barriers in standards, procurement and cost can be overcome. Achieving it would require strong alignment between government and industry on low-carbon outcomes.

Scope

The analysis in this report is based on Infrastructure Australia’s Market Capacity Project Database, including major projects per state, defined as:

- infrastructure projects with a capital value of $100 million or more in New South Wales, Victoria, Queensland, and Western Australia

- infrastructure projects with a capital value of $50 million or more in South Australia, Tasmania, the Australian Capital Territory, and the Northern Territory

- private building projects with a capital value of $25 million or more

- all energy projects, regardless of capital value.

Material quantities

Material quantities were determined from this system, which combines forecast capital expenditure with an overlay of the typical spend on plant, labour, equipment and materials (PLEM) per asset type.

For this report:

- Materials data were the primary source and the basis for calculations in modules A1-A3 and construction waste in module A5.

- Plant data were the basis for construction energy in module A5.

- Labour data were used for construction costs in module A5, where strategies had an influence on labour costs.

- Equipment data were not used.

Emission factor selection and calculation

Emission factors were calculated to represent national or state averages wherever possible. Emission factors were weighted using apparent consumption, as below:

𝐴𝑝𝑝𝑎𝑟𝑒𝑛𝑡 𝑐𝑜𝑛𝑠𝑢𝑚𝑝𝑡𝑖𝑜𝑛 = 𝐷𝑜𝑚𝑒𝑠𝑡𝑖𝑐 𝑝𝑟𝑜𝑑𝑢𝑐𝑡𝑖𝑜𝑛 + 𝐼𝑚𝑝𝑜𝑟𝑡𝑠 − 𝐸𝑥𝑝𝑜𝑟𝑡𝑠

Where there were multiple domestic manufacturers or multiple import countries, emissions were weighted by market share wherever possible. Where this information was not publicly available, plant manufacturing capacity was used as a proxy for market share for domestic manufacture.

Upfront carbon

The analysis in this report focuses on upfront carbon defined here as the greenhouse gas emissions and removals associated with the creation of an asset, network or system up to practical completion. This definition is based on that for ‘capital carbon’ from PAS 2080:2023 (BSI Australia, 2023).

Carbon emissions are calculated as the “sum of greenhouse gas emissions and greenhouse gas removals in a product system, expressed as CO₂-equivalent (CO₂e) and based on a life cycle assessment using the single impact category of climate change” (ISO, 2018). Where the term carbon is used in this report, it refers to the carbon dioxide equivalent (CO₂e) of all greenhouse gases.

Upfront carbon includes the following life cycle modules:

- Modules A1—A3: Manufacture of building products.

- Module A4: Transport of building products to site.

- Module A5: Construction, which includes:

- land use change from land clearing

- construction waste

- construction energy

- commissioning energy.

Figure 12: Lifecycle modules according to ISO 21931-1:2022, highlighting upfront carbon

These lifecycle module codes (i.e., A1-A3, A4 and A5) derive from international and European standards for lifecycle assessment of buildings and infrastructure assets. It is worth noting that many building/infrastructure asset carbon footprint studies do not include commissioning energy. This is an item that emerged as being relevant for some asset types during the stakeholder consultation process for this project. Further, land use change is often excluded due to a lack of good data on its potential impacts. Both are included within this study.

Two analyses for two purposes

This report employs two different calculation approaches for two different purposes:

- The pipeline analysis calculates the emissions embodied in Australia’s pipeline of infrastructure and buildings, as forecast. Calculations are based solely on Infrastructure Australia’s National Infrastructure Project Database, without any scaling. Projects that fall below the thresholds are excluded. Projects are reported in the year they are forecast, without accounting for slippage.

- The hybrid analysis aims to calculate the embodied emissions that occur in a specific year. This is done by filling gaps for building projects under $25 million, by accounting for project slippage where possible and by including a wider range of construction products.

The purpose of the Hybrid Analysis is to demonstrate the significance of embodied carbon relative to Australia’s total national greenhouse gas (GHG) emissions. Its figures are presented as percentages of emissions as well as absolute emissions. By contrast, the Pipeline Analysis is not presented relative to national emissions because the forecast emissions may be spread across more than one year.

Calculation method

Calculating the baseline carbon footprint

The baseline carbon footprint was calculated by summing several elements:

- Manufacture of building products = amount of construction (in $) × material intensity (typically kg per $) × emission factor (typically kg CO₂e per kg).

- Transport of building products to site = amount of construction (in $) × material intensity (typically kg per $) × typical transport distance (in km) × emission factor (typically kg CO₂e per kg·km).

- Land use change from land clearing = total land use change from construction (in kg CO₂e) × construction per typecast (in $) / total amount of construction (in $)

- Construction energy = operation of plant (in $ per type of plant/machine) × energy intensity (e.g., MJ per $) × emission factor (e.g., kg CO₂e per MJ)

- Construction waste = amount of construction (in $) × material intensity (typically kg per $) × waste factor (%) × emission factor (typically kg CO₂e per kg).

- Commissioning energy = amount of energy used for commissioning (in $) × energy intensity (e.g., MJ per $) × emission factor (e.g., kg CO₂e per MJ)

The amount of construction is total dollars per asset type (of which there are 63 types) and per state/territory. In the base analysis for the report (the Pipeline Analysis), the amount of construction comes solely from Infrastructure Australia’s National Infrastructure Project Database. The Hybrid Analysis uses the same data for transport infrastructure and utilities, but bases its buildings data on statistics from the Australian Bureau of Statistics and the Department of Climate Change, Energy, the Environment and Water.

Forecasting emission savings

Identifying decarbonisation strategies

The materials available within Infrastructure Australia’s database were used as the basis for developing an initial longlist of decarbonisation strategies. Strategies were divided into those that affect materials/products (modules A1-A3) and those that affect construction (module A5).

13 decarbonisation strategies were selected (in 11 groups) with different rates and levels of adoption, from an initial longlist of 25 strategies.

Five criteria were used to select decarbonisation strategies:

- MTargets upfront carbon

Only decarbonisation strategies that had the potential to actively reduce upfront carbon were considered. - Like-for-like replacement